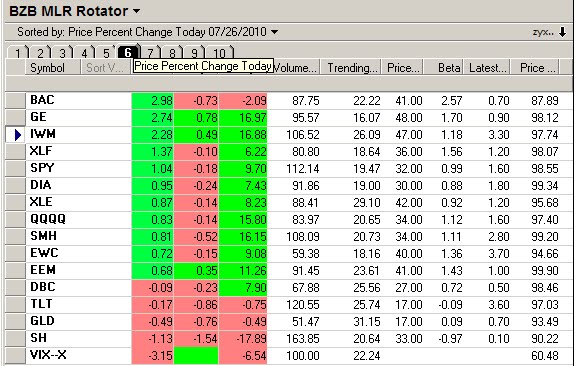

First of all I have no idea how the Rotator came to rank FXY as #1. The chart looks like it's rolling over and although it's had a nice run the technicals suggest there's not much juice left in this one. I might be wrong but FXY goes in the AVOID box for now for me.

On the other hand GDX and by extension SLV look to be picking up as does XLE. FXE is a bit harder to read and seems to still have some doubts about where it should be going . . I'll give that one a little room to breath before jumping in.

The positive tone of last week's earnings reports appears to have given new life to a market that was about to capitulate in the face of deteriorating fundamentals and gloomy Fed forecasts. Always keep in mind that the market is driven by expectations and a tendency to interpret data to suit one's own agenda, which is what make it so much fun (and challenging).

A long standing joke among quants is that 87% of all statistics are made up on the spot and if you read enough Goldman analysts' reports you might come to believe it. GS probably pulled off one of their best trades in the history of the firm by paying a piddling $550 million fine to the SEC to settle claims of that Goldman helped structure a mortgage security that was designed to fail and sold it to unwitting clients.

FYI, $550 million represents 2 weeks worth of GS first quarter profits so the fine is cosmetic at best plus, as part of the settlement GS doesn't have to admit to any wrongdoing. Hey! . . just an honest mistake . . can happen to anybody. Buffett still loves 'em so all's forgiven.