Today I'm kicking off Project Z . . a deconstruction of the

Lazy Man's trading system (retired version), looking at the technical dynamics of each component and considering how other trading systems can complement the simple weekly rotational model to milk a few more dollars from these cash cows while at the same time reining in drawdown.

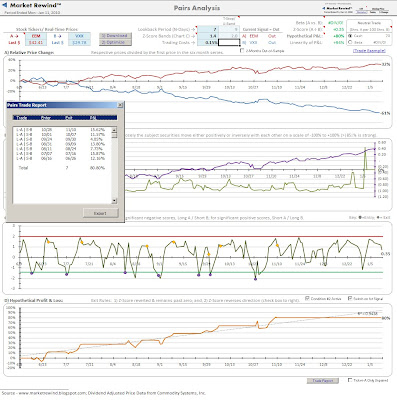

First, over the next few days we'll look at each of the 4 ETFs . . EEM, DBC, QQQQ and SH through the lens of the VXX , the ETN derivative of the VIX that trades like a stock.

Utilizing the

ETF Rewind pairs analysis should help provide a perspective on the relative volatility and technical linearity of each ETF while at the same time detecting the highest probability entries, exits and, perhaps most importantly, holding times.

Today's view is of the EEM and, as with all the current ETF Rewind pair studies, displays pair performance for the past 6 months only. Jeff's made several refinements to the earlier version of the algorithm and its now possible to set separate values for the high and low values of the z score bands and thanks to my constant whining he's added an N day stop that prevents unsuccessful band reversal excursions from progressing very far past the optimized N day value.

In this case that stop is set to 9 days, providing a little breathing room for the reversal but not allowing it to run wild. These 2 little mods improve performance significantly and eliminate all marginal and over extended losing trades.

Over the 6 month test period the system kicked out 7 trades with an average hold time of 7+ days, leaving us with cash about 70% of the time that can be deployed into other momentum candidates.

Note that all the trades are Long A (EEM) and Short B (VXX) and effectively detect positive surges in EEM momentum, which is really what we want to exploit.

Next up . . . my leeettle friend, the Qs.

Thursday's

Thursday's

{kind=link}